S-Reits face worst crisis

After astonishing growth, overall value of units plunges 60 per cent

By Jessica Cheam

(Taken from the Straits Times on the 28th March 2009)Professor James Shilling, a real estate academic from DePaul University in the United States, who believes Reits will experience growth in the long term

'S-Reits have been undergoing the most challenging and difficult times since their inception,' said property giant City Developments' group general manager, Mr Chia Ngiang Hong.

Reits are listed on the stock exchange. They own a property portfolio - shopping malls, for instance - and make regular payments to unit-holders.

Investors piled into Reits, attracted by the reliability of payments and the good yields. Reits grew at an astonishing rate - their combined market value hit $33.5billion in June 2007 from just $740million in 2003, Mr Chia noted.

However, the global crisis and tight credit markets have contributed to a market free-fall for Reits.

Overall, the value of Reit units has plunged by about 60per cent, said National University of Singapore (NUS) provost Tan Eng Chye.

Both Mr Chia and Professor Tan were speaking at the NUS Department of Real Estate's public forum on S-Reits yesterday.

Refinancing and recapitalisation risks are the darkest clouds hanging over the industry, said the real estate department's Associate Professor Sing Tien Foo.

An estimated $4.6billion in S-Reit debt is due to be refinanced this year. Another $12billion is due next year, he said.

The weak financial markets and elevated risks among lenders have made it difficult to get financing.

Given their structure, Reits are heavily dependent on capital markets, said Moody's senior analyst Kathleen Lee.

The industry will see a wave of consolidation, and smaller Reits are at greater risk of having refinancing issues.

Some here may even go under, she added, citing a case in Japan where New City Residence Reit sought court protection late last year with US$1.1billion (S$1.6billion) in debt.

Moody's, along with other rating agencies, has in recent months downgraded the credit ratings of many S-Reits.

One scenario that might emerge from this crisis could be firms with the 'smart money' acquiring weaker Reits and taking them private, said Mr Philip Levinson of the Asian Public Real Estate Association.

The association last month asked the Government to help Reits refinance an estimated $12 billion of debt.

It was reported that one request was to lower the minimum investor payout ratio that Reits must meet to qualify for tax transparency treatment - from the current 90per cent to as low as 50per cent.

This has since been rejected by the authorities, on the grounds that the characteristics of Reits as a stable, high-payout, pass-through vehicle are important considerations for investors.

At the panel discussion yesterday, rights issues also came under fire.

CapitaMall Trust had recently issued units at a hefty discount to market price, drawing criticism that this was an expensive source of capital to refinance debts.

Ms Lee said even though this is true, a rights issue is an available option to raise cash and will be the 'only way to go' for some as a matter of survival.

She added that besides refinancing risks, Reits are also rated on their portfolio diversity, quality of assets and track records of its management.

Guest speaker James Shilling, an established real estate academic from DePaul University in the United States, told the 150-strong forum audience that despite the current weak performance of Reits, he believed 'Reits are here to stay' and will experience growth in the long term.

In the meantime, Reits are in for a tough and volatile time ahead.

'When the volatility index comes down, investors will come back and that's when things will start turning a corner,' he said.

Ms Lee added that she believed the recovery will be a 'lazy L-shaped' one, where it will take some time before the market recovers fully.

jcheam@sph.com.sg

Sunday, March 29

Saturday, March 28

Dividend Discount Model

2 comments

I have been thinking hard about the different discounting methods of valuing stocks. Valuing stocks is to find the intrinsic value of the stock and this is one of the main pillars of investing since the objective is to purchase stocks which are at a significant discount to their intrinsic value. Currently, I am using price to earnings ratio to value stocks since I believe that there are advantages to using this method over the discounting methods such as the factoring of the market's behavior which can be irrational at times.

The two most common methods so far are the discounted cash flow which in short, stands for DCF and the dividend discount model which in short, stands for DDM. So far, I am favouring the DDM over DCF because it appears to be more realistic although it depends on how you use the formulas. The formulas are only as good as the numbers itself, thus if you input garbage into the formula, your answer is likely to be as good as your input. The formula for DDM is given as below.

In other words, the value of the stock is the present value of the sum of all the dividends that you are going to receive in the future til perpetuity. However, this seems to be not very realistic. That is because, I don't buy a stock simply for the the dividends itself. The reason I buy a stock is due to the potential for capital gains due to price appreciation and dividends. Thus, I will sell the stock when it appears to be overvalued and this is often the time when I can lock in on my potential gains. In other words, the value of a stock to me is the present value of all the dividends that I am going to receive plus the selling price of the stock in the future. Thus I should discount the dividend individually and the selling price of the stock back to its present value.

For example, let's use the STI ETF as an example. For a start, I will need to find the dividend and the expected selling price of the STI ETF in the future. Currently, the STI ETF distributes a dividend of $0.10 per share. Let's make a conservative assumption that this dividend will be the same for the next 5 years.

For the selling price in the future, I am expecting to sell the STI ETF in 5 years time at a price of $4.50. This is because going by past instances, the average time for the STI to recover from its bottom is 2.6 years and the longest instance was around 5 years. Furthermore, the previous 3 peaks of the STI occurs at 3875.77, 2582.94 and 2137.99 so a target of 4500 in 5 years time should be quite conservative. Lastly, a discount rate of 10% is chosen to be used with the formula or you can see it as the required rate of return that you want from buying the STI ETF is 10%. Thus we will discount the dividend for each of the year for 5 years and the selling price of the STI ETF at the end of five years. The computation is given below.

Thus the value of the STI ETF is at $3.17. Since the current price is around $1.75, this means that it is at a significant discount to the value that will give you a rate of return of 10%. This would mean that the STI ETF would be a good buy at its current price. This computation can also be applied to other stocks too.

Wednesday, March 25

They pay money to learn to make money

7 comments

They pay money to learn to make money

Financial training courses in demand despite volatile markets; experts warn against get-rich-quick mindset

By Joanna Seow

(Taken from the Straits Times on the 23rd March 2009)THEY claim to teach you how to become a millionaire, retire rich or even make 'lots of money' during a recession.

Whatever the claims, eager participants are lining up for financial training courses, not in the least put off by the economic slump or plunging share markets.

These courses are not cheap - fees range from around $2,000 to more than $7,000 for anywhere from two to eight days of coaching - but the lure of trading riches overrides the cost. Companies say the recession has not dampened demand, with 40 people turning up on average - whether retirees, self-employed, students or managers - all looking for an edge.

Courses usually specialise in a particular market, such as stocks, foreign exchange (forex) or options.

'Each option contract controls 100 shares, so option trading is low risk, yet gets high returns,' said one organiser.

'The forex market has tremendous volume and is open 24 hours a day,' enthused another.

Or, 'the US stock market has over 14,000 listed companies for you to choose from, and it's tax-free'.

While the hooks differ, most courses have one thing in common: selling strategies to help people get the most they can out of financial markets - and at a time when every extra dollar counts.

The training goes further than simply teaching from a textbook, and coaches focus on money management, psychological aspects of trading and software usage.

Sceptics, of course, will cite the old adage: 'Those who can, do; those who can't, teach'.

Mr Chris Firth, the chief executive of wealth management firm dollarDEX, is one. He is 'very dubious about these courses' and feels that if traders are really so brilliant, they will be spending more time trading rather than training other people.

Yet customers still roll up. At the three free course previews attended by The Straits Times, there were people with trading experience and those without. Most were keen to find ways to boost their income or even switch to full-time trading.

Administrator Diana Woo, 34, said: 'Now that the economy is so bad, I want to see how I can get more money to supplement my income.' She has done some share trading in the past, and was at a preview for a forex course.

As course organisers are quick to point out, getting some coaching should not be seen as a get-rich-quick scheme.

Mr Ee Chee Koon, the chief trainer and chief operating officer of Asia Charts, said people desperate for instant cash should not turn to trading, as the wrong mindset could be dangerous.

'A man came to me in desperation in 2007 after losing 50 per cent of his retirement fund in bad trades,' he said. 'He had followed poor advice from someone else. I told him to cool down before starting to trade again, because his psychology would be very weak.'

Investing in a share trading course in January proved worthwhile for area information technology manager Jason Kwok, 38, who recouped the $2,900 he spent on the Asia Charts course within a month and recommended the course to four friends.

Full-time trader Eric Lye, 36, also thinks he got enough bang for his buck. He used to earn a five-figure monthly income at a bank, but after attending a T3B Holdings forex trading course last year, he was able to earn the same or more from trading.

Ms Karen Loh, a marketing manager with a multinational corporation, was also highly impressed with the T3B course she attended last September, which set her back by about $2,500.

The 36-year-old said: 'The training was thorough and comprehensive, and constant support is provided even after the course through teaching gatherings on Saturdays and an online forum.'

She had attended another forex course, which was a disappointment.

'Many people think they can just go for a course, then start trading on their own without any support, but it's actually very tough,' she said.

People should also be wary of trainers who misrepresent their qualifications, like Mr Clemen Chiang of Freely Business School. He claimed to have a doctorate in option trading but was exposed as getting the degree from an unaccredited university. This month, the Small Claims Tribunal awarded participants of his trading seminars partial refunds of course fees.

Most people told The Straits Times that courses should teach how to invest wisely, including in volatile times like now. They also want continuous after-course support, such as daily coaching, weekly discussion sessions or online trading forums and newsletters.

But skill and nerve come into it as well. Mr Clarence Chee, a forex trader and a coach with T3B, said many people who trade are losing money or are too scared of the risks involved.

'People need to understand that with the right strategies, the risk is manageable,' he said.

Frankly, I am skeptical of such trading courses. The line of reasoning is very simple. If the trading strategies and systems that they are employing are indeed that profitable, why would they offer to teach others ? Surely, trading will be much more lucrative than conducting courses.

If they wish to help the public in improving their finances through trading, I think charging a few thousand per head for each course is more than enough to cover the cost of the courses over a few times round. It would be far more cheaper to read some technical analysis and trading books and subsequently, paper trade for a while to see trading is workable for you. If not, it won't be too late anyway to go for such courses.

I am not doubting the abilities of these traders and since I have not use any of their trading systems or strategies before, I'm not in any position to judge actually. Among the people who attended such courses, there will definitely be people who will become successful traders but I believe they are the minority.

Now this reminds me of investing. If you realize, there are trading courses being advertised online. A flip to the money section of the Straits Times and you can probably see that quite a lot of advertisements in that section are promoting trading courses. So far, I hardly come across any investing courses yet. Perhaps investing is not as appealing as trading ? Anyone wonders how did Warren Buffett ends up as the 2nd richest person on this planet currently ?

Saturday, March 21

Balance Sheet

No comments

A balance sheet is a statement that summarize the assets, liabilities and the shareholder's equity of a company. It is useful in helping us to determine the financial position of a company. In this post, I will be using the balance sheet of M1, which is a local telecommunications company. The balance sheet can be seen in the picture below.

The balance sheet can be dividend into 3 parts and these 3 parts are assets, liabilities and equity. So what are these items ? Assets are anything of value, liabilities are debts while equity is the portion of the assets that belongs to the shareholders. These 3 items are related by the following equation.

The balance sheet can be dividend into 3 parts and these 3 parts are assets, liabilities and equity. So what are these items ? Assets are anything of value, liabilities are debts while equity is the portion of the assets that belongs to the shareholders. These 3 items are related by the following equation.

Assets = Liabilities + EquitySo what is the rationale behind this equation ? Let me explain using an example below.

You wish to buy a car that has a value of $50,000. However, you only have $20,000. Thus you decide to go to a bank to take a loan of $30,000. As a result, you are able to purchase the car. In this case, you took on a loan of $30,000 thus you will have a liability of $30,000 while the other $20,000 came from your pocket, so this $20,000 will be your equity. In all, you will own a car that has a value of $50,000 thus you will have an asset of $50,000.Similarly, the stockholders of a company contributes capital to a company and the company may take on additional debts to fund the purchase of assets which can help the company to increase its earnings. I have grouped the assets, liabilities and equity with coloured rectangular boxes on M1's balance sheet. The blue stands for the assets, red stands for the liabilites and the green one stands for the equity. In my next post, I will be discussing on what each individual item on the balance sheet stands for.

Thursday, March 19

Sunday, March 15

Wednesday, March 11

STI Technical Analysis 11th Mar

No comments

STI has fallen below the support level of 1473 made on the 28th of October last year. I expect that there will be more downside to come.

STI has fallen below the support level of 1473 made on the 28th of October last year. I expect that there will be more downside to come.

CPF and HDB Loan

12 comments

Currently, CPF contributions to your Ordinary Account can be used to pay for your monthly mortgage payment of your flat. If you are taking the HDB concessionary loan, the interest rate of this loan is pegged at 0.1% above the interest rate in the CPF Ordinary Account. The current base interest rate of the CPF Ordinary Account stands at 2.5% thus the interest rate of the HDB concessionary loan is at 2.6%. However, do remember that the 1st $20,000 in your CPF Ordinary Account earns 3.5% and that is higher than the interest rate of the HDB concessionary loan. Given the higher interest rate for the CPF Ordinary Account as compared to the HDB Concessionary Loan, should you transfer your excess funds in your CPF Ordinary Account to reduce your HDB concessionary loan, especially if you are buying your first HDB flat ?

Currently, CPF contributions to your Ordinary Account can be used to pay for your monthly mortgage payment of your flat. If you are taking the HDB concessionary loan, the interest rate of this loan is pegged at 0.1% above the interest rate in the CPF Ordinary Account. The current base interest rate of the CPF Ordinary Account stands at 2.5% thus the interest rate of the HDB concessionary loan is at 2.6%. However, do remember that the 1st $20,000 in your CPF Ordinary Account earns 3.5% and that is higher than the interest rate of the HDB concessionary loan. Given the higher interest rate for the CPF Ordinary Account as compared to the HDB Concessionary Loan, should you transfer your excess funds in your CPF Ordinary Account to reduce your HDB concessionary loan, especially if you are buying your first HDB flat ?

Since the interest rate for the 1st $20,000 in your CPF Ordinary Account is higher than the interest of the HDB Concessionary Loan, it would not be prudent to transfer the funds from your CPF Ordinary Account to pay off part off your housing loan as the yield earned on the CPF Ordinary Account is higher than the interest expense of the housing loan. In the past, the interest rate of the CPF Ordinary Account was only 2.5% thus if you transfer the funds from your CPF Ordinary Account, you can save the difference in 0.1% since the interest of the HDB Concessionary Loan is at 2.6% although the difference is not that significant. With the special interest rate of 3.5% on your 1st $20,000 in your CPF Ordinary Account, this is no longer true.

Currently, CPF contributions to your Ordinary Account can be used to pay for your monthly mortgage payment of your flat. If you are taking the HDB concessionary loan, the interest rate of this loan is pegged at 0.1% above the interest rate in the CPF Ordinary Account. The current base interest rate of the CPF Ordinary Account stands at 2.5% thus the interest rate of the HDB concessionary loan is at 2.6%. However, do remember that the 1st $20,000 in your CPF Ordinary Account earns 3.5% and that is higher than the interest rate of the HDB concessionary loan. Given the higher interest rate for the CPF Ordinary Account as compared to the HDB Concessionary Loan, should you transfer your excess funds in your CPF Ordinary Account to reduce your HDB concessionary loan, especially if you are buying your first HDB flat ?

Currently, CPF contributions to your Ordinary Account can be used to pay for your monthly mortgage payment of your flat. If you are taking the HDB concessionary loan, the interest rate of this loan is pegged at 0.1% above the interest rate in the CPF Ordinary Account. The current base interest rate of the CPF Ordinary Account stands at 2.5% thus the interest rate of the HDB concessionary loan is at 2.6%. However, do remember that the 1st $20,000 in your CPF Ordinary Account earns 3.5% and that is higher than the interest rate of the HDB concessionary loan. Given the higher interest rate for the CPF Ordinary Account as compared to the HDB Concessionary Loan, should you transfer your excess funds in your CPF Ordinary Account to reduce your HDB concessionary loan, especially if you are buying your first HDB flat ?Since the interest rate for the 1st $20,000 in your CPF Ordinary Account is higher than the interest of the HDB Concessionary Loan, it would not be prudent to transfer the funds from your CPF Ordinary Account to pay off part off your housing loan as the yield earned on the CPF Ordinary Account is higher than the interest expense of the housing loan. In the past, the interest rate of the CPF Ordinary Account was only 2.5% thus if you transfer the funds from your CPF Ordinary Account, you can save the difference in 0.1% since the interest of the HDB Concessionary Loan is at 2.6% although the difference is not that significant. With the special interest rate of 3.5% on your 1st $20,000 in your CPF Ordinary Account, this is no longer true.

Furthermore, there is one important benefit to leaving some funds behind in your CPF Ordinary Account and this benefit is an intangible one. The benefit is that the funds can be used as a buffer to pay your monthly mortgage payment if the contribution to your CPF is stopped due to any unfortunate circumstances such as retrenchment. For example, the contribution to your CPF Ordinary Account is just enough to pay off your monthly mortgage payment. Unfortunately, you have been retrenched due to the downsizing of your company thus the contributions to your CPF accounts will be stopped. As such, you will have to fork out cash to pay for your monthly mortgage payment and the last thing you will want to do is to fork out more cash to pay for this as you have lost your source of employment income. Thus it will be beneficial to leave excess funds in your CPF Ordinary Account.

Monday, March 9

SIBOR and SOR Links

4 comments

I realized that quite a lot of visitors who arrived at this site are looking for the daily SIBOR and SOR, thus I have added links to the daily SIBOR and SOR. The links to the daily SIBOR and SOR are located at the right column of this site under 'Useful Links'.

Upon clicking the link to the daily SIBOR, you will arrive at the Asian Bonds Online website. Under the Market Watch, look for Interest Rates. You should see the 3 Month SGD SIBOR there.

To see the SIBOR for other time periods, proceed to the 'click here for all markets'. Subsequently, a pop-out window should appear. Under the local currency reference rates, click on the next market until you see SIBOR.

As for the SOR, the link will bring you to the website of the Mortgage and Finance Association of Singapore. The daily SOR and the SIBOR for the different time period will be listed on the main page. I hope this will prove to be useful. If there are any better links to the daily SIBOR and SOR, it will great if you can let me know about it.

Upon clicking the link to the daily SIBOR, you will arrive at the Asian Bonds Online website. Under the Market Watch, look for Interest Rates. You should see the 3 Month SGD SIBOR there.

To see the SIBOR for other time periods, proceed to the 'click here for all markets'. Subsequently, a pop-out window should appear. Under the local currency reference rates, click on the next market until you see SIBOR.

As for the SOR, the link will bring you to the website of the Mortgage and Finance Association of Singapore. The daily SOR and the SIBOR for the different time period will be listed on the main page. I hope this will prove to be useful. If there are any better links to the daily SIBOR and SOR, it will great if you can let me know about it.

Thursday, March 5

Dividend Yield and Investing

7 comments

The understanding of the concept of yield can be a good guide in helping us to make investment decisions. In general, you should always try to invest in assets when it can give you a good yield and vice versa. This seems like an easy thing to do but it is often not so straightforward. Let me illustrate with an example using stocks.

Let us consider Singapore Technologies Engineering Limited which is listed on SGX as ST Engg. A look at the dividend history reveals that it gave out a dividend of $0.1711 per share in 2007 and $0.1788 per share in 2008.

Dividend yield is simply given dividend divided by price in terms of percentage. Let us now consider the price history of ST Engg. The highest and the lowest price of ST Engg in 2007 is $3.98 and $3.18 while the highest and the lowest price of ST Engg in 2008 is $3.65 and $1.99. To make things simple, let us define the average closing price of ST Engg to be the average of the highest and lowest closing price. Thus the average closing price of ST Engg is $3.58 for 2007 and $2.82 for 2008.

Let us then compute the average dividend yield by using the dividend and divide it by the average closing price.

The average dividend yield in 2007 will be $0.1711/$3.58*100% = 4.78%

The average dividend yield in 2008 will be $0.1788/$2.82*100% = 6.34%

It can be seen that a lower price will enable us to receive a higher dividend yield and vice versa. Thus by taking the yield into consideration, it can help us in making decisions on investments. As such, you should buy stocks when the dividend yield is attractive and vice versa.

Taking this into consideration, attractive yields can only be achieved when stock prices are low and that often happens in a bear market. This is often the time when most of us would hesitate to put our funds into the stock market due to fear and pessimism. However, if you think along the line of trying to get a good dividend yield, this will often be the best time to invest in the stock market logically.

However, this line of reasoning should only be applied to stocks of fundamentally strong companies or ETF that track stock indices. The reason is because such companies are more likely to be giving out dividends in times of recession and poor economic outlook as compared to fundamentally weak companies in general. As for ETFs, the companies that consist of the stock indices which the ETFs are tracking, are likely to be fundamentally strong companies with large capitalization.

Let us consider Singapore Technologies Engineering Limited which is listed on SGX as ST Engg. A look at the dividend history reveals that it gave out a dividend of $0.1711 per share in 2007 and $0.1788 per share in 2008.

Dividend yield is simply given dividend divided by price in terms of percentage. Let us now consider the price history of ST Engg. The highest and the lowest price of ST Engg in 2007 is $3.98 and $3.18 while the highest and the lowest price of ST Engg in 2008 is $3.65 and $1.99. To make things simple, let us define the average closing price of ST Engg to be the average of the highest and lowest closing price. Thus the average closing price of ST Engg is $3.58 for 2007 and $2.82 for 2008.

Let us then compute the average dividend yield by using the dividend and divide it by the average closing price.

The average dividend yield in 2007 will be $0.1711/$3.58*100% = 4.78%

The average dividend yield in 2008 will be $0.1788/$2.82*100% = 6.34%

It can be seen that a lower price will enable us to receive a higher dividend yield and vice versa. Thus by taking the yield into consideration, it can help us in making decisions on investments. As such, you should buy stocks when the dividend yield is attractive and vice versa.

Taking this into consideration, attractive yields can only be achieved when stock prices are low and that often happens in a bear market. This is often the time when most of us would hesitate to put our funds into the stock market due to fear and pessimism. However, if you think along the line of trying to get a good dividend yield, this will often be the best time to invest in the stock market logically.

However, this line of reasoning should only be applied to stocks of fundamentally strong companies or ETF that track stock indices. The reason is because such companies are more likely to be giving out dividends in times of recession and poor economic outlook as compared to fundamentally weak companies in general. As for ETFs, the companies that consist of the stock indices which the ETFs are tracking, are likely to be fundamentally strong companies with large capitalization.

Wednesday, March 4

Banks cut interest rates for deposits

2 comments

Banks cut interest rates for deposits

Move follows Sibor's plunge and reflects flush conditions in money markets, analysts say

By Gabriel Chen(Taken from The Straits Times, 3rd March 2009)

BANK depositors are again feeling the pinch as a key interest rate continues to plunge, further squeezing the meagre returns on their savings.

At least four banks - Maybank, Standard Chartered Bank (Stanchart), United Overseas Bank (UOB) and OCBC Bank - have trimmed their rates for deposits or are set to do so.

This follows further hefty falls in the rate banks pay one another to borrow cash, known as the Singapore Interbank Offered Rate (Sibor) - a key influence on the rate that banks pay depositors.

The Sibor is hovering at just 0.68 per cent, bringing it near the all-time low of 0.56 per cent reached in June 2003. It has plunged about 70 per cent from 2.22 per cent last September. Since early January, when it was about 0.97 per cent, the rate has nose-dived about 30 per cent.

This month, OCBC is slashing the interest rate paid on its FairPrice Plus Account from 1 per cent to 0.5 per cent for the first $50,000, but will still pay 1 per cent for amounts higher than that. It used to pay 1 per cent a year for this account, with no minimum balance requirement.

'In the light of declining Sibor rates, banks have started aligning the interest rates for savings accounts downwards,' said OCBC's head of customer segment and portfolio management, Ms Lee Ee Ling.

With margins under pressure, other banks have responded by also trimming rates for customers.

Last month, Maybank cut rates for iSAVvy, an online savings account, from 1.08 per cent to 0.5 per cent a year, provided there is a daily balance of $5,000 to below $50,000.

Stanchart's rate for its eSaver online savings product is 0.4 per cent a year, down from the 0.5 per cent it paid in early January for deposits under $50,000.

Come March 16, the rates paid on UOB's i-Account, Campus Account and FlexiDeposit Account will be cut. The new rates, made public last month, are available on the bank's website.

For example, its FlexiDeposit Account, a statement- based savings account, will fall from 0.35 per cent to 0.25 per cent for the first $15,000.

Barclays Capital economist Leong Wai Ho has predicted: 'Sibor will continue to set new lows this year.

'This is a reflection of extremely flush conditions in the money markets, as a safe hedge against the worsening global backdrop and dislocated credit markets.'

OCBC Bank economist Selena Ling said the US Federal Reserve has cut its Fed funds target rate to a range of 0 per cent to 0.25 per cent, and is now 'considering alternative quantitative easing measures'. The Sibor closely tracks this rate.

Bankers have not ruled out further falls in deposit rates, to as low as 0.l25 per cent, in the near future.

If that seems implausible, think again. In early 2003, POSB savings and passbook account-holders received 0.125 per cent for the first $50,000.

Today, Singdollar deposits yield at least 0.25 per cent.

'Most Singapore banks do not have a competitive reason to attract deposits,' said the head of a foreign bank.

'Due to capital constraints, not many are in an expansionary mode in terms of more lending or increasing their asset book, therefore, there are...fewer reasons to attract deposits for funding purpose.'

The falling Sibor should, in theory, benefit new home buyers taking up Sibor-linked housing loans, but in reality they may not be better off. This is because many banks are raising the spreads they charge above Sibor.

At DBS, for example, a home buyer taking out a loan of 80 per cent of his property's value last July would have paid the Sibor rate plus 1.25 percentage points. Now, a new buyer has to pay Sibor plus 1.75 percentage points.

'Banks are making huge margins now between deposit and lending rates. Banks feel they have to be compensated for taking the risk on loans,' a banker said.

DBS, OCBC and UOB all saw quarter- on-quarter improvement in net interest margins during their fourth-quarter results announced last month.

Net interest margins measure the difference between what banks pay for deposits and borrowings and what banks earn on loans and investments.

gabrielc@sph.com.sg

Sunday, March 1

Survival of the Fittest

1 comment

"It's only when the tide goes out that you learn who's been swimming naked."

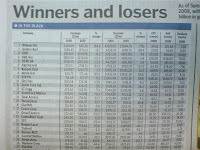

There was a useful article in the Money section of the Straits Times today. It summarizes the net profits and their turnover of the companies listed on SGX along with their NAV i.e. Net Asset Value per share and EPS i.e. Earnings per share. My apologies for the blur images as I don't have a scanner so I took the pictures using my camera phone instead. It is only during times like these where we can see which are the stronger and fundamentally better companies that are still able to increase their revenue and profits despite the recession. This reminds me of a classic Warren Buffett quote.

"It's only when the tide goes out that you learn who's been swimming naked."

Warren Buffett

Some of the companies that you should keep a lookout for includes those companies which are still able to boost their turnover and earnings. Another thing to look out is those companies that are selling below their NAV as this essentially means that they are selling below than their worth.

There were a few surprises on the list for me and one of such surprises was DBS. The NAV of DBS as listed in the table is $12.48 and going by its latest closing price of $8.04, it is selling at a discount of around 35% and I find it to be rather pessimistic.

Subscribe to:

Comments (Atom)