CPF to extend 4% interest in SMRA accounts until 31 Dec 2011

Taken from Channelnewsasia on the 20th September 2010

SINGAPORE : The government has decided to further extend the 4 per cent floor or minimum rate for interest on CPF savings for the Special, Medisave and Retirement Accounts (SMRA) for another year until 31 December 2011 .

This is the second time that it has been extended.

Explaining the move in a statement, Manpower Minister Gan Kim Yong, said that despite Singapore's strong economic recovery, interest rates have remained low this year.

He added that the sharp drop in interest rates at the expiry of the 4 per cent floor rate may impact CPF members who may not have benefited fully from the economic recovery yet.

Since January 2008, SMRA savings have been invested in 10-year Government Securities plus 1%.

This is a market-based rate for instruments of comparable risk and duration, and will ensure that members receive fair and reasonable interest rates.

However, to help members cope with the transition, the government had committed to providing a 4 per cent floor rate for SMRA interest for two years up to December 2009.

This was extended to December 2010, in light of the global economic conditions and exceptionally low interest rate environment a year ago.

Beginning 2012, the interest rates will be subject to a minimum rate of 2.5 per cent per annum. - CNA /

Tuesday, September 21

Friday, September 17

Sibor drops to record 0.51%

1 comment

Sibor drops to record 0.51%

By Gabriel Chen

Taken from The Straits Times, 16 Sep, 2010

By Gabriel Chen

Taken from The Straits Times, 16 Sep, 2010

A key Singapore interest rate that determines some mortgage rates has sunk to a new record low, offering the prospect of even cheaper home loans.

The rate at which banks here lend to one another – the three-month Singapore Interbank Offered Rate, or Sibor – is now 0.51 per cent.

It has been hovering around the mid-0.5 per cent levels for the past few months.

In September 2008, it spiked to 2.22 per cent, as banks were afraid to lend to one another for fear of not getting repaid during the global credit crunch.

Sibor, which also affects rates for consumer loans and deposit rates, has been sliding of late.

This has been in line with the trend of interest rates set by the United States Federal Reserve, which are at historic lows. The Fed is continuing its strategy of trying to kick-start the anaemic US economy with cheap credit.

The record Sibor low also comes as the Singapore dollar has been allowed to strengthen since April.

Asia, including Singapore, is seeing major capital inflows, and this puts more liquidity into the system than would otherwise have been the case. The flushed liquidity conditions then puts downward pressure on rates.

A number of banks here offer mortgages with interest rates that are pegged to the Sibor, so there are cheaper home loans in store for homebuyers.

Still, some banks have widened the spreads that they charge above the Sibor.

This reduces the impact that the falling Sibor will have on Sibor-linked packages.

‘Still, by and large, people will be paying less for Sibor-pegged loans,’ noted Mr Nicholas Tan, OCBC Bank’s head of global wealth management.

In the low interest rate environment, some banks have introduced new housing loan products that are undercutting the rates offered by their competitors.

Maybank Singapore, for example, last month launched a new range of home loan products with interest rates that start at below 1 per cent, which is one of the lowest in town.

This intensifying fight for market share based on pricing is causing some bankers here to be concerned.

‘We are afraid of another price war breaking out,’ said a senior banker.

‘With Singapore cooling its real estate market and banks fighting for fewer real estate deals, we are looking at competition being more price intensive.’

But Ms Vibha Coburn, Citibank Singapore’s business director for secured finance, said that even if a price war breaks out, banks are not obliged to take part.

‘I don’t see the necessity of being in a price war,’ she said.

Ms Coburn said banks will have promotions from time to time, but when rates are so low, homebuyers will consider other factors, such as the turnaround time for a loan application.

‘Assuming all the customer’s documents are in place, we can give him the letter of offer in an hour,’ she said.

The low interest rates will not be a ‘pivotal factor’ to attract homebuyers back to the market, said Mr Nicholas Mak, executive director of research and consultancy at SLP International.

He said current home prices and the expected future pricing of properties are more important factors.

Some buyers are expecting prices to drop further and are holding off on making purchases, after the Government recently implemented further measures to cool speculation.

But while consumers benefit from the lower Sibor, it will mean continued lean times for those with bank deposits.

The soft Sibor is also restricting how much Singapore banks, which are net lenders on the interbank market, can charge on new loans.

This hurts their net interest margins, which measure how profitable their lending activities are.

Standard Chartered economist Alvin Liew has been revising his three-month Sibor forecast downwards, projecting rates to be at 0.5 per cent by the end of next year, from 1.5 per cent in his previous forecast.

‘The risk is that there might be more downside revision,’ he said.

The rate at which banks here lend to one another – the three-month Singapore Interbank Offered Rate, or Sibor – is now 0.51 per cent.

It has been hovering around the mid-0.5 per cent levels for the past few months.

In September 2008, it spiked to 2.22 per cent, as banks were afraid to lend to one another for fear of not getting repaid during the global credit crunch.

Sibor, which also affects rates for consumer loans and deposit rates, has been sliding of late.

This has been in line with the trend of interest rates set by the United States Federal Reserve, which are at historic lows. The Fed is continuing its strategy of trying to kick-start the anaemic US economy with cheap credit.

The record Sibor low also comes as the Singapore dollar has been allowed to strengthen since April.

Asia, including Singapore, is seeing major capital inflows, and this puts more liquidity into the system than would otherwise have been the case. The flushed liquidity conditions then puts downward pressure on rates.

A number of banks here offer mortgages with interest rates that are pegged to the Sibor, so there are cheaper home loans in store for homebuyers.

Still, some banks have widened the spreads that they charge above the Sibor.

This reduces the impact that the falling Sibor will have on Sibor-linked packages.

‘Still, by and large, people will be paying less for Sibor-pegged loans,’ noted Mr Nicholas Tan, OCBC Bank’s head of global wealth management.

In the low interest rate environment, some banks have introduced new housing loan products that are undercutting the rates offered by their competitors.

Maybank Singapore, for example, last month launched a new range of home loan products with interest rates that start at below 1 per cent, which is one of the lowest in town.

This intensifying fight for market share based on pricing is causing some bankers here to be concerned.

‘We are afraid of another price war breaking out,’ said a senior banker.

‘With Singapore cooling its real estate market and banks fighting for fewer real estate deals, we are looking at competition being more price intensive.’

But Ms Vibha Coburn, Citibank Singapore’s business director for secured finance, said that even if a price war breaks out, banks are not obliged to take part.

‘I don’t see the necessity of being in a price war,’ she said.

Ms Coburn said banks will have promotions from time to time, but when rates are so low, homebuyers will consider other factors, such as the turnaround time for a loan application.

‘Assuming all the customer’s documents are in place, we can give him the letter of offer in an hour,’ she said.

The low interest rates will not be a ‘pivotal factor’ to attract homebuyers back to the market, said Mr Nicholas Mak, executive director of research and consultancy at SLP International.

He said current home prices and the expected future pricing of properties are more important factors.

Some buyers are expecting prices to drop further and are holding off on making purchases, after the Government recently implemented further measures to cool speculation.

But while consumers benefit from the lower Sibor, it will mean continued lean times for those with bank deposits.

The soft Sibor is also restricting how much Singapore banks, which are net lenders on the interbank market, can charge on new loans.

This hurts their net interest margins, which measure how profitable their lending activities are.

Standard Chartered economist Alvin Liew has been revising his three-month Sibor forecast downwards, projecting rates to be at 0.5 per cent by the end of next year, from 1.5 per cent in his previous forecast.

‘The risk is that there might be more downside revision,’ he said.

Thursday, September 16

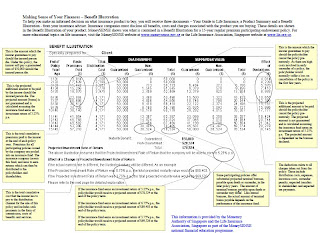

Looking deeper into the benefit illustration

1 comment

Moneysense has a excellent explanation of the benefit illustration but I thought it would be good to explain on how are the numbers are derived.

(Taken from moneysense.gov.sg)

Moneysense has a excellent explanation of the benefit illustration but I thought it would be good to explain on how are the numbers are derived.

This benefit illustration is an example of a 15 years regular premium participating endowment policy. As you may know, the premiums after accounting for the expenses will go into a participating fund or in short, a par fund in which the insurer will manage this fund to in order to grow it. This participating fund is also used for payouts to those who make claims on their policies.

For this benefit illustration, the investment return is assumed to be at 5.25%. The surrender value is the amount which you will get back if you terminate the policy. And this surrender value is made up of 2 components, the guaranteed and the non-guaranteed portion. Once again, the non-guaranteed portion is subjected to the investment performance of the fund and this is not guaranteed while the guaranteed portion is the portion which the insurer is obligated to give you back.

End of 1st year

If the entire premium paid is invested,

$3814 * 105.25% = $4014

Since the surrender value for the end of 1st year is zero, you will lose $4014 if you surrender the policy. This figure corresponds with the figure given under the effect of deductions.

End of 2nd year

Premium paid for 1st year is invested for another year,

$4014 * 105.25% = $4225

Premium paid for 2nd year is invested.

$3814 * 105.25% = $4014

Total return for 2nd year,

$4225 + $4014 = $8239

Since the surrender value for the end of 2nd year is zero, you will lose $8239 if you surrender the policy. This figure corresponds with the figure given under the effect of deductions.

End of 3rd year

Premium paid for 1st year is invested for another year,

$4225 * 105.25% = $4447

Premium paid for 2nd year is invested for another year,

$4014 * 105.25% = $4225

Premium paid for 3rd year is invested,

$3814 * 105.25% = $4014

Total return for 3rd year,

$4447 + $4225 + $4014 = $12686

Since the surrender value for the end of 3rd year is $6766, you will lose $12686 - $6766 = $5920 if you surrender the policy. This figure corresponds with the figure given under the effect of deductions. Notice that the surrender value of $6766 consists of the guaranteed portion of $6494 and the non-guaranteed portion of $272.

For the remaining years, one can use a spreadsheet to work out the numbers since it is quite repetitive.

There are a couple of things you should take note when it comes to the benefit illustration. The first thing is that you should always take the projected investment return with a pinch of salt. Insurers may have a tendency to use a higher projected investment return to make the numbers look nicer. As such, it is always prudent to ask yourself if the projected investment return is realistic. That is because, such a plan represents a long term financial commitment and it may be detrimental to your financial plans if the insurer fails to meet the projected returns down the road. Perhaps, the easiest way is to look at the guaranteed amount of the surrender value since this is the amount that the insurer must give it to you if you terminate your policy. In this case, the guaranteed portion of the surrender value is always less than the total premiums paid. Neglecting the time value of money, you may have to think for yourself whether this policy is a good one.

Another thing is that the death benefit in endowment plans is likely to be not enough to cover your insurance needs. If you have a few dependents who depends on your income to survive, a death benefit of a few grands will probably be enough to last them a few years only. As such, you cannot use such plans to cover the needs of your dependents in the event that you pass away.

Subscribe to:

Comments (Atom)